In China, domestic PP producers succeeded in marginally expanding margins, while PE market sentiment turned more upbeat with some fresh gains in the week ended April 26 . A slight increase in futures prices combined with falling domestic inventory levels has mostly boosted prices. Meanwhile, some restocking ahead of the Golden Week holiday from May 1 to May 5 supported the latest price uptrend.

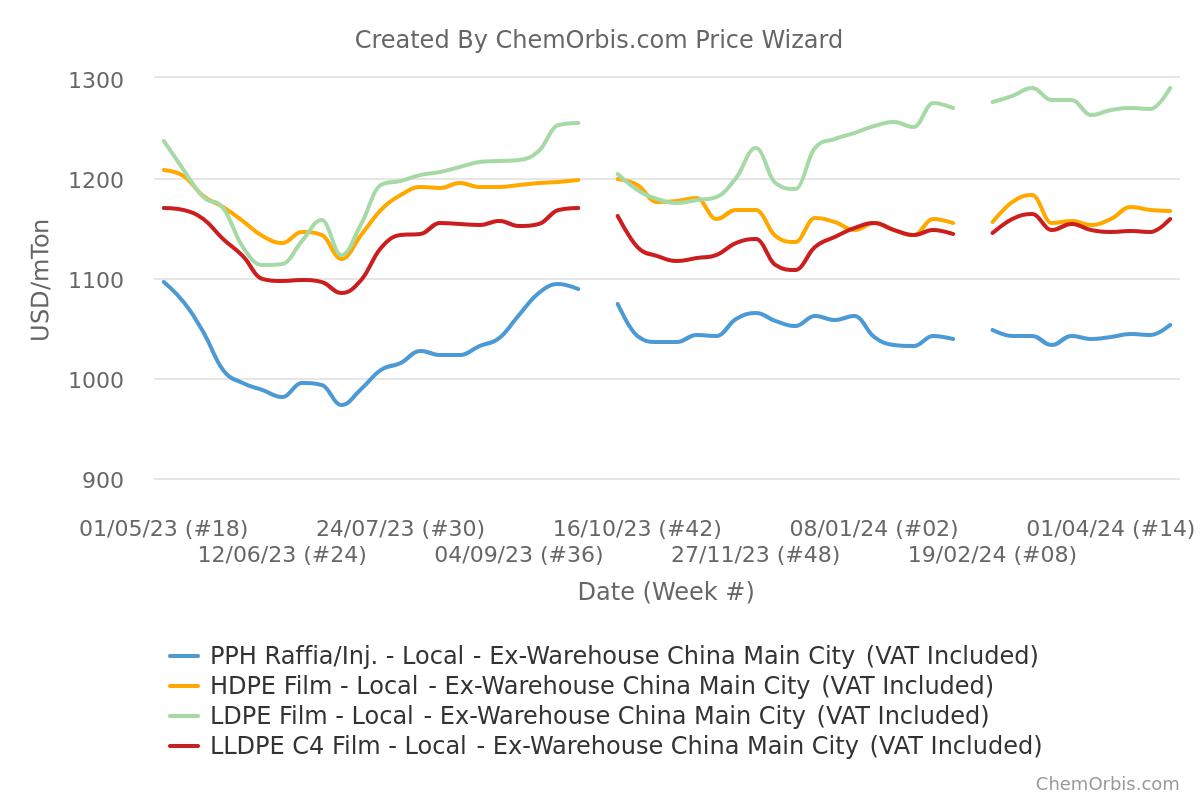

LDPE prices led the upward trend, reaching their highest level in more than a year

During the week ending April 26, domestic LDPE film prices led the upward trend across China’s domestic polyolefin markets. According to data from ChemOrbis Price Index, after the latest increase of CNY 150-160/ton ($21-22/ton), the weekly average price of domestic LDPE film in USD terms has increased to a high level. most since mid-March 2023.

Meanwhile, HDPE film remains the weakest of the three major PE film grades, although sellers have tried to boost prices after offering some downward revisions last week.

For PP, the general domestic price range is estimated to increase by 50-100 CNY/ton (7-14 USD/ton) to 7500-7750 CNY/ton (917-947 CNY/ton excluding VAT) for PP homo raffia and inj. and stable or increased by 100 CNY/ton (14 USD/ton) to 7700-7900 CNY/ton (941-966 USD/ton excluding VAT) for PPBC inj., all by warehouse method, Cash includes VAT. According to the ChemOrbis Price Index, weekly average prices for both hit their highest levels in nearly four months.

Domestic inventories decreased by 7% compared to the previous week

The heavy maintenance season in Q1 and Q2 played a key role in the ongoing decline in China’s domestic polyolefin supply, paving the way for sellers to test the market by raising prices. Sustained export orders, especially for PP, also eased concerns about domestic supply, according to market participants.

“Domestic prices continue to move higher amid tight supply in Eastern and Southern China, where most factory maintenance is taking place,” said a converter. Recent maintenance by domestic manufacturers has contributed to the ongoing decline in manufacturing capacity utilization.”

According to market sources, the total polyolefin inventories of the two major domestic producers stood at 750,000 tons on April 26, showing a marked decrease of 55,000 tons, or nearly 7%, from the previous week. Domestic inventories continued to decrease every week after the Qingming Festival.

However, market participants have approached current market conditions with caution, as supply remains abundant. A domestic trader said: “Domestic and foreign sellers are trying to increase prices but the release of domestic inventory is slow and supply pressure continues.”

Another market participant added: “Currently, there is no supply pressure on petrochemical inventories. However, it is anticipated that inventory pressure will increase after the holidays, with inventories expected to accumulate to approximately 900,000 tons.”

Pre-holiday demand appears, albeit limited

Adding to the reduction in supply was a slight increase in purchasing demand ahead of the extended Golden Week holiday, with demand coming from plastic textile products, film packaging applications as well as food and beverage packaging.

Meanwhile, market participants noted that pre-holiday demand fell short of expectations as buyers continued to focus on essential purchases. Another trader said: “Demand growth is limited, most downstream converters are buying to meet urgent demand. High raw material prices reduce their profit margins, leading to low purchasing demand.”

Volatility in futures and upstream markets is in the spotlight

Although PP and PE producers remain under cost pressure, recent volatility in Dalian oil and futures prices has impacted the trading atmosphere. “The downward trend in crude oil prices has weakened the ability to support costs, while futures contracts have fallen, affecting the spot market,” said a market source.

After previous price drops, crude oil prices slid down and remained below the threshold of 90 USD/barrel. However, Brent oil futures recorded an increase of nearly 1 USD/barrel in the latest trading session, while the benchmark price increased further and was listed at 89.30 USD/barrel at the time of writing.

September PP and LLDPE futures prices on the Dalian Commodity Exchange recorded weekly declines of 34 CNY/tonne (5 USD/ton) and 63 CNY/ton ($9/ton) as of the 25th. April. Meanwhile, both futures contracts increased again to 61-93 CNY/ton. (8-13 USD/ton) in the trading session on April 26.

Written by Thi Huong Nguyen – thihuongnguyen@chemorbis.com